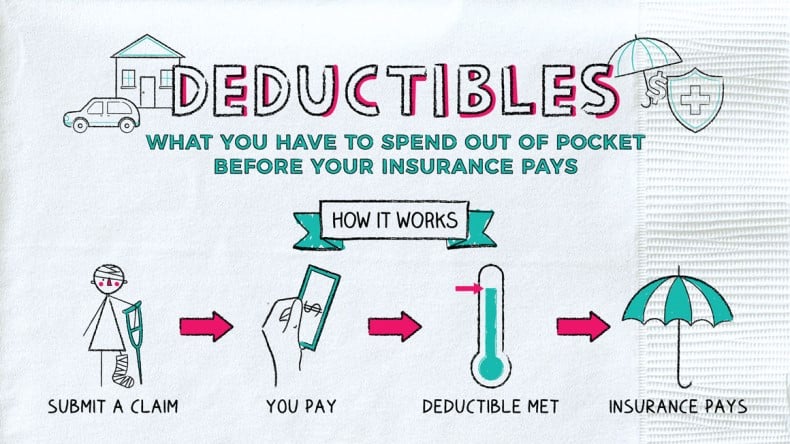

An insurance deductible is the amount of money you, as the policyholder, are responsible for paying out of pocket before your insurance coverage kicks in to cover the remaining costs. Deductibles are a common feature in various types of insurance policies, including health insurance, auto insurance, homeowners insurance, and others.

Here’s how insurance deductibles typically work:

- Selection of Deductible Amount:

- When you purchase an insurance policy, you often have the option to choose a deductible amount. Deductibles can vary and are specified in the insurance policy.

- Out-of-Pocket Payment:

- If you make a claim covered by your insurance policy, you are required to pay the deductible amount first before the insurance company contributes to the remaining costs. This means you are responsible for the initial portion of the covered expenses.

- Insurance Coverage:

- After you’ve paid the deductible, your insurance coverage becomes active, and the insurance company will pay the agreed-upon percentage or amount of the remaining covered costs, up to the policy limits.

- Example:

- For example, if you have an auto insurance policy with a $500 deductible and you’re involved in an accident resulting in $2,000 in damages, you would pay the first $500 (deductible), and the insurance company would cover the remaining $1,500, assuming the damages are within the policy limits.

- Annual Deductible:

- Some insurance policies have an annual deductible, which means the deductible amount applies over the course of a year. Once you’ve met the annual deductible, your insurance coverage may cover additional claims within that year without requiring further deductible payments.

It’s important to carefully review your insurance policy to understand the specific terms and conditions related to deductibles, as they can vary between policies and insurance providers. The amount of the deductible can affect your insurance premiums, with higher deductibles often leading to lower premium costs and vice versa.

In summary, an insurance deductible is the initial amount you must pay out of pocket before your insurance coverage takes effect. It serves as a way to share the financial responsibility between the policyholder and the insurance company.

is insurance deductible based on the date of service?

The insurance deductible is typically based on the date of service or the date when a covered event occurs. In various types of insurance, such as health insurance or auto insurance, the deductible is applied to expenses or losses that occur during a specific period.

Here are a few examples:

- Health Insurance:

- In health insurance, the deductible is often applied on a calendar year basis. For example, if your health insurance has an annual deductible of $1,000, it means you are responsible for paying the first $1,000 of covered medical expenses in a given calendar year. Once you’ve met the annual deductible, the insurance coverage may begin to pay a portion of the remaining covered costs.

- Auto Insurance:

- In auto insurance, the deductible is typically applied to each covered incident. If your auto insurance policy has a $500 deductible and you’re involved in a covered accident, you would be responsible for paying the first $500 of the repair costs. This deductible usually resets for each new covered incident.

- Property Insurance:

- For property insurance, such as homeowners or renters insurance, the deductible may apply to each covered claim. If your home suffers covered damages and you have a $1,000 deductible, you would be responsible for the initial $1,000 of repair costs, and the insurance coverage would apply to the remainder, up to the policy limits.

It’s important to check the specific terms and conditions of your insurance policy to understand how the deductible is applied and whether it is based on a specific period (e.g., calendar year) or per covered event. Insurance policies can vary, and the deductible structure is outlined in the policy documents provided by the insurance company. If you have questions about your insurance deductible, it’s recommended to contact your insurance provider directly for clarification.

Why is my insurance deductible so high?

Several factors can contribute to why your insurance deductible may be high. The deductible amount is often determined by a combination of factors, and it can vary based on the type of insurance coverage you have. Here are some reasons why your insurance deductible might be high:

- Policy Type and Coverage:

- The level of coverage you choose can impact your deductible. Comprehensive coverage with a lower deductible often comes with higher premiums. If you opt for a policy with a high deductible, it may result in lower premium costs.

- Risk Factors:

- Insurance companies assess risk factors when determining deductibles. If you are considered to be at higher risk for filing claims, such as having a history of accidents or a lower credit score (in some cases), the insurance company may set a higher deductible.

- Insurance Company Policies:

- Different insurance companies have varying policies and pricing structures. Some companies may offer policies with higher deductibles as a way to provide more affordable premiums. It’s essential to shop around and compare quotes to find the balance between deductible and premium that suits your needs.

- Type of Insurance:

- The type of insurance you have can influence the deductible amount. For example, health insurance policies often have annual deductibles that reset each year, while auto insurance deductibles are typically applied per covered incident.

- Policy Customization:

- When you customize your insurance policy, such as adding optional coverage or adjusting coverage limits, it can affect your deductible. Additional coverage options or lower coverage limits may result in a higher deductible.

- Location:

- Your geographical location can impact insurance costs, including deductibles. If you live in an area with higher rates of accidents, crime, or natural disasters, insurance companies may set higher deductibles to account for increased risk.

- Personal Choices:

- Choices you make when selecting your policy, such as opting for a higher deductible to reduce monthly premiums, can result in a higher out-of-pocket expense when a claim is filed.

If you find that your insurance deductible is too high for your comfort, you may have the option to adjust it by contacting your insurance provider. Keep in mind that changing your deductible may affect your premium, so it’s essential to carefully evaluate the trade-offs between deductible and premium costs based on your financial situation and risk tolerance. Additionally, working with an insurance agent or broker can help you explore options that align with your needs and budget.

can insurance deductibles be claimed on taxes?

As of my last knowledge update in January 2022, the ability to claim insurance deductibles on taxes depends on the type of insurance and the purpose of the insurance coverage. Generally, personal insurance premiums and deductibles are not deductible on individual income tax returns for federal income tax purposes. However, there are specific circumstances where certain insurance-related expenses may be deductible. Here are a few considerations:

- Medical Expenses:

- If you itemize deductions on your federal income tax return, you may be able to deduct qualified medical expenses, including certain health insurance premiums and out-of-pocket costs like deductibles. However, there are limitations, and only expenses that exceed a certain percentage of your adjusted gross income (AGI) are deductible. The threshold is typically 7.5% of your AGI, but it’s subject to change, so it’s essential to check the current tax laws.

- Business and Rental Property Insurance:

- If you have a business or own rental property, insurance premiums and related expenses for these activities may be deductible as business expenses. Deductibility can vary based on the nature of the insurance and how it relates to the business or property.

- Casualty and Theft Losses:

- In certain cases, casualty and theft losses may be deductible. This could include losses covered by insurance, but the deduction is generally limited to losses that are not compensated by insurance or other means.

- Flood Insurance:

- The cost of flood insurance for a personal residence may be deductible if the property is in a federally designated flood zone. However, this deduction is specific to flood insurance.

Tax laws are subject to change, and it’s important to consult with a tax professional or refer to the most recent tax regulations for the specific year you are filing. Tax rules can vary by jurisdiction, and deductions depend on individual circumstances.

Always consult with a qualified tax advisor or accountant to ensure you are taking advantage of any available deductions based on your unique situation and the most current tax laws.

what is the difference between a deductible and a premium in an insurance policy?

In an insurance policy, the deductible and the premium are two distinct components that policyholders need to understand. They play different roles in how insurance coverage operates, and they impact the cost and structure of the policy. Here’s a breakdown of the key differences between a deductible and a premium:

- Deductible:

- Definition: A deductible is the amount of money that the policyholder is responsible for paying out of pocket before the insurance coverage kicks in to cover eligible expenses.

- Purpose: Deductibles are designed to share the financial responsibility between the policyholder and the insurance company. It helps prevent small or routine claims and encourages policyholders to be mindful of their usage of the insurance.

- Payment: The deductible is paid by the policyholder when a covered claim is made. For example, if you have a $500 deductible on your auto insurance and you incur $1,000 in covered damages, you would pay the first $500, and the insurance company would cover the remaining $500.

- Premium:

- Definition: A premium is the amount of money that the policyholder pays to the insurance company for coverage. It is typically paid on a regular basis, such as monthly, quarterly, or annually.

- Purpose: Premiums are the primary cost of insurance coverage. They represent the amount the policyholder pays to maintain and access the benefits of the policy.

- Payment: Premiums are paid by the policyholder according to the agreed-upon schedule. The amount of the premium is determined by various factors, including the type and amount of coverage, the policyholder’s risk profile, and other considerations.

Key Differences:

- Financial Responsibility:

- Deductible: The deductible is the initial amount the policyholder must pay for covered expenses before insurance coverage applies.

- Premium: The premium is the ongoing cost paid by the policyholder to maintain insurance coverage.

- Frequency of Payment:

- Deductible: Paid when a covered claim is made.

- Premium: Paid regularly (e.g., monthly, quarterly, annually).

- Purpose:

- Deductible: Encourages responsible use of insurance and prevents overuse for minor expenses.

- Premium: Covers the cost of providing insurance coverage.

In summary, the deductible is the amount the policyholder pays before insurance coverage begins, while the premium is the ongoing cost paid to maintain the insurance policy. Both elements contribute to the overall structure and cost of an insurance policy.

what is the highest deductible for car insurance in California?

As of my last knowledge update in January 2022, I don’t have specific information on the highest deductible for car insurance in California because insurance policies and regulations can change, and specific details can vary among insurance providers. Deductibles for car insurance are typically determined by the insurance company and can vary based on factors such as the type of coverage, the policyholder’s driving history, the make and model of the vehicle, and other considerations.

If you’re looking for information on car insurance deductibles in California, I recommend contacting insurance providers directly or using online tools provided by insurance companies. You can request quotes and explore different deductible options based on your preferences and needs.

Keep in mind that insurance regulations and offerings can change, so it’s essential to check with insurance providers for the most up-to-date and accurate information. Additionally, consulting with an insurance agent or broker can be helpful in understanding the various deductible options and how they may impact your overall insurance coverage and costs.